Driven by a desire to improve the comfort and experience of hotel guests and meet company sustainability standards, the Hilton Los Angeles/Universal City hotel invested in a $7 million deep retrofit in 2014. The Property Assessed Clean Energy, or PACE, funding mechanism provided long-term, non-recourse, off-balance-sheet financing for upgrades to the HVAC system and controls, elevators, chillers, lighting and other equipment. The project added $335,000 in net operating income in year one and increased the estimated value of the property by more than $30 million.

other words, standard practice can lead to underinvestment in a valuable commodity.

In anticipation of a new regulation to decrease energy consumption, the French government’s Caisse des Dépôts et Consignations (CDC) established a process to optimize energy retrofit investments through consideration of asset values. The analysis examined the correlation between higher-energy-use buildings and vacancy periods between leases, as well as differences in rental and exit values. As part of this analysis, CDC estimated a deep retrofit of a 1930s-era building in the Paris Central Business District would increase asset value by 10 percent. The analysis resulted in the decision to move forward with the deep retrofit of the building, which is now completely retrofitted and commercialized.

These stories corroborate strong market evidence that energy-cost savings, while significant, represent just one driver motivating investment in deep-energy retrofits, or building retrofits that employ an integrated array of energy conservation measures to reduce energy consumption by 30 percent or more.

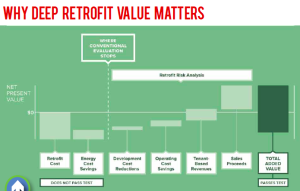

To date, investment in deep-energy retrofits has been limited in large part by an insufficiently compelling business case. Investments made in energy efficiency today typically have to provide a 30 percent return on investment (a 3 1/2-year payback) based on energy-cost savings alone. Some deep-energy retrofits approach or clear this hurdle, but many do not.

Real-estate investors generally neglect the value beyond energy-cost savings—values highlighted by the previous stories—when they prepare and present capital requests for deep retrofits. The result: undervaluation of deep retrofit opportunities that leads to (unintended) underinvestment in efficient buildings, leaving millions on the table—and increasing carbon emissions in the atmosphere.

Incorporating the additional—albeit less tangible—value beyond energy-cost savings into decision-making is therefore critical to improving investor due diligence, enabling better assessments of the value proposition for deep retrofits, and, in turn, unlocking needed capital.