Going Beyond Energy-cost Savings

In April, Rocky Mountain Institute (RMI), which has locations in Snowmass and Boulder, Colo., released a new practice guide for real-estate investors to capture all value beyond energy-cost savings resulting from the execution of a deep retrofit project and address the failure of the market to fully recognize this value. The guide provides a comprehensive deep retrofit value methodology and complements the 2014 report RMI produced for owner-occupants. (See retrofit’s May-June 2014 issue, page 18.)

The guide is useful to those interested in better understanding how energy-efficiency retrofits create value for class A and B office buildings and better estimating this value. The basic value framework presented can also be applied, with adjustment, to other property types, including residential properties, new construction, tenant improvements and equipment replacements. Investors who use the methodology presented in the guide can improve their assessment of deep retrofits during capital planning, leading to more informed decision-making and better allocation of capital.

Calculating and presenting five key sources of value beyond energy-cost savings (provided on page 20) will help unveil the often overlooked benefits of investing in deep-energy retrofits—and promote increased investment:

1. Retrofit Capital Costs: Retrofit projects can have little cost premium if timed with other capital-improvement projects and if they take advantage of subsidies and other financial incentives, such as tax credits or subsidized lending.

2. Non-energy Operating Costs: Deep retrofits can reduce operating costs associated with maintenance, insurance and occupant churn rate, as well as increase occupied space through equipment downsizing and improved occupant use of space. In some cases, mechanical, server and other support spaces can be completely eliminated; this has been a major driver of value for deep retrofits in space-constrained, high-cost markets like New York City.

3. Tenant Revenues: Retrofits can enhance demand, resulting in increased rents, occupancies, absorption and tenant retention. Calculation of the value derived from tenant-based revenues can be accomplished with an industry-standard discounted cash-flow analysis.

4. Sales Revenues: Sales revenue premiums from deep retrofits result from higher net operating income, increased investor demand and risk reduction.

5. Retrofit Risk Analysis: The thorough identification and evaluation of risks enables action to mitigate and accurately price them, helping to maximize value from the other value elements.

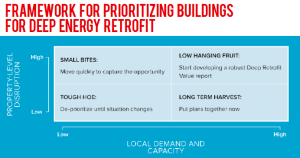

Figure 1 illustrates how accounting for deep retrofit value reveals an improved business case.